In This Issue:

Editors Welcome: The Invisible Hand of Innovation

Federal Budget SR&ED Changes: Dollars and Cents

Mergers & Acquisitions in the Food and Beverage Industry

Despite Turbulent Economy, Canadian Companies Plan to Move Ahead with IPOs

Are You Ready for Stormy Weather?

Editors Welcome:

The Invisible Hand of Innovation

Written by:

Ela Malkovsky, Technical Writer and Editor-in-Chief

Ela Malkovsky

B.A.

Instrumental in the growth of a company, and the economy as a whole, is the role of competition, quietly and persistently benefiting society through individual ambitions to maximize gains in the marketplace.

Ela is dedicated to supporting the advancement of Canadian companies by identifying and leveraging innovative research and technology based funding options.

According to the 2012 OECD (Organisation for Economic Co-operation and Development) Economic Survey of Canada, competitive pressures that spur innovation have recently intensified because of the high exchange rate. Adapting to increased economic pressures to compete in the current global marketplace requires creative solutions to common business problems. More often than not, innovation occurs through small, incremental improvements to existing concepts that result in exponential savings to the company, savings that can be reinvested into innovation, commercialization and growth.

Take for example the introduction of the assembly line, which revolutionized the manufacturing process by significantly cutting costs to production, thereby allowing resource intensive products like cars to become affordable. Although many companies at the time were working to develop the assembly line and the concept of a division of labour was not new, Henry Ford and the Ford Motor Company were the first to master the moving assembly line, pressured by the high costs of manufacturing technology in an emerging sector and fuelled by the belief that competition is the keen cutting edge of business, always shaving away at costs (Henry Ford).

Launched in a converted factory in 1903 with $28,000 in cash from twelve investors, Ford Motor Company produced just a few cars a day, with two or three men working on each car. Within a decade, the company would become a world leader in the assembly line concept, having innovated existing workforce concepts and developed creative solutions to the same issues that their competitors were facing. Similarly, the narrowing competitive margins of the current global economy are putting pressure on companies to improve their methods and reduce costs in order to secure their position in the marketplace.

In welcoming you to the summer newsletter of 2012, we have provided several articles to advance your knowledge of government funding and financing assistance to increase your competitive edge. We thank you for your support and wish you a very productive summer!

North Consulting Group is dedicated to providing full-service strategic insights and resources to help you attain your business objectives. It is currently comprised of: NorthBridge Consultants (R&D tax credit consulting); NorthLink Capital Advisors (mergers & acquisitions, capital raising and succession planning advice); NorthSpring Capital Partners (providing risk capital to privately-held businesses); and North Innovation Fund (SR&ED accrual debt financing).

Federal Budget SR&ED Changes:

Dollars and Cents

Written by:

James Ro, Vice President of NorthBridge Consultants

The 2012 Federal Budget was released this past March and included some relatively significant changes to the SR&ED program in Canada. What was interesting in the Jenkins Report (released Oct 2011) was that its recommendations were focused on changes that would impact Small and Medium-sized Enterprises (SMEs), whereas the Federal Budget ended up favouring SMEs (see details below). This didnt come as much of a surprise as the majority Conservative government had a mandate to reduce the deficit and according to the Jenkins Report, large enterprises represented approximately 60% of the SR&ED tax credits granted but only approximately 10% of the total number of claimants in 2007. As a result, the government met their political agenda by reducing government spending and focusing on the bigger dollars, but at the same time, did not upset the approximate 20,000 SME claimants in a meaningful way i.e., remained popular with the voting masses.

James has over 10 years of experience in a wide range of business areas, including SR&ED, management, debt and equity financing, mergers, acquisitions and divestitures.

You can do a Google search and find a lot of literature summarizing the 2012 Federal Budget changes, but are claimants clear on what the changes mean to their bottom line in terms of dollars and cents? I have attempted to provide generic numerical examples of the SR&ED program changes in the tables below to demonstrate the dollar impact on claims for both SMEs (referred to as CCPCs) and large or foreign enterprises (referred to as Non-CCPCs).

In summary:

- For both CCPCs and Non-CCPCs, the proxy will be reduced from 65% to 55% of salary base.

- For both CCPCs and Non-CCPCs, subcontractor costs will be reduced from 100% to 80% of eligible subcontract expenses.

- For both CCPCs and Non-CCPCs, SR&ED capital equipment will no longer be eligible (this will not impact many SME claimants, as capital is not a common expenditure for smaller companies).

- For CCPCs, the general ITC rate will remain unchanged.

- For Non-CCPCs, the general ITC rate will be reduced from 20% to 15%.

In the example below, the Non-CCPC can expect to see an almost 40% reduction in their Federal ITC; whereas the CCPC can expect their Federal ITC to decrease only by approximately 7%.

| CCPC - Illustrative Calculation of Total SR&ED Expenditures | |||

|---|---|---|---|

| Current | Projected | Variance % | |

| Labour/Wages(T4) | 600,000 | 600,000 | |

| Proxy - % of T4 Labour | 65% | 55% | |

| Proxy Amount | 390,000 | 330,000 | -15% |

| Materials | 100,000 | 100,000 | |

| Subcontractor - % | 100% | 80% | |

| Subcontractor - $ | 100,000 | 80,000 | -20% |

| R&D Capital Equip - % | 100% | 0% | |

| R&D Capital Equipment | - | - | 0% |

| Total Expenditures | 1,190,000 | 1,110,000 | -7% |

| General ITC Rate | 35% | 35% | |

| Assumed Federal Tax Credit | 416,500 | 388,500 | -7% |

| Non-CCPC - Illustrative Calculation of Total SR&ED Expenditures | |||

|---|---|---|---|

| Current | Projected | Variance % | |

| Labour/Wages(T4) | 600,000 | 600,000 | |

| Proxy - % of T4 Labour | 65% | 55% | |

| Proxy Amount | 390,000 | 330,000 | -15% |

| Materials | 100,000 | 100,000 | |

| Subcontractor - % | 100% | 80% | |

| Subcontractor - $ | 100,000 | 80,000 | -20% |

| R&D Capital Equip - % | 100% | 0% | |

| R&D Capital Equipment | 150,000 | - | -100% |

| Total Expenditures | 1,340,000 | 1,110,000 | -17% |

| General ITC Rate | 20% | 15% | |

| Assumed Federal Tax Credit | 268,000 | 166,500 | -38% |

While much more extensive reductions were discussed; only a portion of these were implemented. Overall, when you combine the revised SR&ED program with other government programs and corporate tax incentives, Canada continues to provide generous, broad-based incentive programs to support R&D and innovation.

If you would like to know more about how the changes to the SR&ED program will affect your claim, please feel free to contact me at (519)623-2486 ext. 227.

Mergers & Acquisitions in the Food and Beverage Industry

Written by:

James Ro, Vice President of NorthBridge Consultants

Canadian M&A activity in the Food & Beverage industry should continue in the latter part of 2012 as the conditions that supported deal-making in the last 12 months remain in place. Supported by large cash accumulations and access to cheap debt, purchasers (especially strategic ones) should continue to seek growth via acquisitions in an environment of subdued economic recovery.

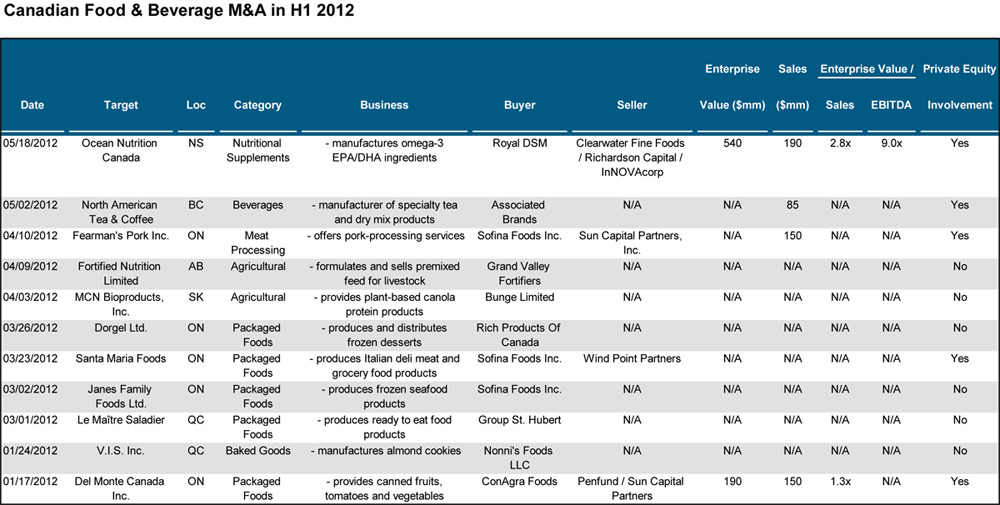

It is important to note that private equity funds continue to be offered attractive debt terms from senior lenders for high-quality deals. Furthermore, they are collectively sitting on significant amounts of un-invested capital on the sidelines. Something that you may not know, private equity funds have five years from their funding raising date to invest their committed capital before they have to return the funds back to investors. As such, the longer they wait and approach their five-year time horizon, the more they will be motivated to acquire companies. Having said that, four out of the eleven Canadian Food & Beverage M&A transactions in the last six months had a private equity firm as the seller - please see the M&A table (click here to view) for further details. While the deal flow in this sector over the last six months confirms a steady M&A market, I do not think there will be a significant increase in M&A activity any time soon.

{kind=link}

James has over 10 years of experience in a wide range of business areas, including SR&ED, management, debt and equity financing, mergers, acquisitions and divestitures.

A Closer Look - Royal DSM Acquires Ocean Nutrition Canada

Target Description: Nova Scotia-based, Ocean Nutrition Canada is the world's largest supplier of Omega-3 EPA/DHA ingredients to the dietary supplement and food manufacturing markets. It was founded in 1997 and has over 400 employees.

Buyer Description: With over 22,000 employees globally and €9 billion in sales, Royal DSM is a global science-based company active in health, nutrition and materials. The acquisition of Ocean Nutrition Canada is its fifth acquisition in the Nutrition segment since September 2010.

Deal Overview: Royal DSM acquired Ocean Nutrition Canada from Clearwater Fine Foods and its private equity investors, Richardson Capital and Innovacorp.

Deal Structure: all-cash deal.

Deal Metrics:

- Total Enterprise Value (TEV - equity plus net debt): $540M

- Expected F2012 sales: $190M

- Expected F2012 EBITDA: $60M

- TEV/F2012 sales: 2.8 times

- TEV/F2012 EBITDA: 9.0 times

Deal Rationale:

- Highly complementary to DSMs successful Martek acquisition in 2011.

- Strengthens and complements DSMs global Nutritional Lipids growth platform, based on healthy, polyunsaturated fatty acids (PUFAs).

- Extends DSMs portfolio of omega-3 fatty acids.

- The Nutritional Lipids category is still at an early stage (yet well established) and offers significant growth opportunities across a broad range of market segments and applications.

James' Comments:

Generally speaking, it is not typical for a Buyer to offer the Seller a premium valuation of more than 6 times EBITDA (Earnings Before Interest, Taxes, Depreciation and Amortization) as Ocean Nutrition Canada received from Royal DSM (9 times EBITDA). There are only a few reasons when this would happen:

- For strategic (market share, diversification, etc.) and/or competitive (defensive, intellectual property, etc.) reasons.

- High profit margins and strong cash flows (including potential cost synergies).

- Significant future growth projections.

It should be noted that Ocean Nutrition Canada had an average annual growth of approximately 20% over the past 5 years. On the surface, the market sees a valuation of 9 times but if you are privy to the buyers details and understand what they bring to the table (distribution, infrastructure, etc.), in addition to the positive industry dynamics, you can start to understand where the valuation metrics come from.

NorthLink Capital Advisors is NorthBridges sister company specializing in mergers & acquisitions, raising capital and succession planning. For more information, please contact James Ro at james@northlinkcapital.com

Despite Turbulent Economy,

Canadian Companies Plan to Move Ahead with IPOs

Written by:

Blair Roblin, Managing Director of NorthLink Capital Advisors

According to Bloomberg, Canadian companies raised $790 million in IPOs during the first five months of the year, representing a 25% decline from the same period a year ago and the lowest since 2008. Challenges have come from Europes debt crisis, while falling commodity prices have also kept companies out of the market.

But the outlook for Canadian IPOs appears to be improving, despite the slow start to the year. This may seem a bit surprising, especially since the lazy days of summer have never been the best for new issues and Canadian stocks have generally been selling off in the past few months. The headlines from the recent Facebook IPO certainly havent helped much either. Nevertheless, companies are anticipating growing investor appetite for yield-oriented offerings, and some private-equity firms are looking to trim their holdings of private firms. This may be a sign that companies are coming around to the fact that the current economic state is the new normal and that financing decisions cannot be put off indefinitely.

Blair has worked in the field of mergers, acquisitions and corporate finance for over 25 years. His advisory roles have been primarily with mid-sized Canadian firms, in a variety of industries.

In all, more than $1 billion could be raised in the next few months if the planned IPOs are successful. The candidates to raise money include two REITs (Real Estate Investment Trust), a casino company, an energy trust and a mining company.

The first of these to launch, HealthLease Properties REIT, has already been successful on June 6th, selling 11 million units at C$10 each and yielding a substantial 8.5%. HealthLease will use the proceeds to buy seniors housing and care properties in Western Canada and the U.S. Midwest. A second REIT, Pure Multifamily, is expected to raise $20 million but this may increase if there is strong interest from retail investors.

Casino operator Gateway Casinos is expected to raise more than $100 million, with about $77 million going towards the repayment of term loans and another $60 million to redeem notes. The issue is being sold by its private equity owners.

Argent Energy Trust recently delayed its marketing by a week after the oil price took a tumble, but the company still expects to finish marketing by the end of June. Argent hopes to be the third new energy trust to trade in Toronto, following a model that shields foreign assets from the tax increases imposed by the federal government in 2006. The company owns U.S. energy assets and is looking to raise $325 million.

Finally, base metal mining company, Intergeo, which is backed by Russian billionaire Mikhail Prokhorov is expected to list in Toronto by the end of the year. Intergeo is a Russian copper and nickel company hoping to raise between C$100 million and C$500 million. The companys chairman and 20% stakeholder, has indicated that the company would float about 10% of its shares in the offering.

The Gateway and Intergeo IPOs should be large enough to rank among the largest IPOs of 2012. Together with Argent, HealthLease and Pure Multifamily, they should prove that the equity markets in Canada are a good place to raise capital, even in these turbulent times.

Are You Ready for Stormy Weather?

Written by:

Brain Hunter, President of NorthSpring Capital Partners

Where is our economy headed? Will European contagion affect our markets? Is the US going over a fiscal cliff of huge tax increases and spending cuts? These are all great questions; I wish I had answers. What I do know is that businesses need to be ready to quickly react to rapidly changing circumstances.

The key to being able to quickly react is having a strong balance sheet that is able to withstand financial shocks. Now is the time to play defensive and ensure you have plenty of working capital and availability under your line of credit. If your business is losing money, pay close attention to your debt to equity and debt service ratios. Be proactive and rebuild your shareholders' equity to maintain bank covenants before your bank takes action.

Lately, we have seen some really creative examples of how to raise additional working capital. One company did a customer assessment which involved the customer making a loan to the company repayable from discounts against future purchases. In a slightly different twist of this, another company received a long term loan from a customer in exchange for guaranteed supply of finished product.

Brian has more than 30 years of experience in providing debt and equity financing to privately-held businesses in Southern Ontario. He earned his BA in Economics and MBA at the University of Western Ontario.

Restoring or improving profitability can be more challenging than improving liquidity. Again, we have seen some interesting solutions recently. One company engaged productivity improvement consultants and, over a six month engagement, this resulted in over $1 million in cost savings, representing 4-5% of revenues. Another company increased their SR&ED claim by over $100,000 after NorthBridge Consultants reviewed the previous consultants draft report and found missing projects and claimable expenditures.

We are also seeing more radical solutions involving mergers, acquisitions and divestitures. A prime example is in the printing industry, which is ripe for consolidation as too many printers are offering the same services to a stagnant market. As advisors, we recently participated in the merger of three printers. Significant synergies and cost savings resulted, and top line revenue growth was achieved by being able to offer expanded services to a larger geographic market. All of the owners that participated expect superior results than as standalone operators.

There are many more financial and strategic buyers than sellers in todays market. Most companies have recovered from the financial crisis of 2008-2009. With attractive low interest rates and risk capital readily available, now is an excellent time for business owners to consider their exit options and timing. If we get into stormy weather these conditions may not be repeated.

You have received this newsletter because of your interest in North Consulting Group. If you feel this has been sent to you in error, you can unsubscribe. While we endeavor to ensure accurate information through this newsletter, it is not a definitive analysis of legislation, or a substitute for professional advice. Please seek professional advice if attempting to relate specific situations to the information disclosed within.

North Consulting Group

Problem Solvers. Independent Thinkers. Optimal Solutions.

Head Office

445 Thompson Drive

Cambridge, ON N1T 2K7

Atlantic Canada | Western Canada | Toronto

The North Consulting Group consists of:

NorthBridge Consultants

NorthLink Capital Advisors

NorthSpring Capital Partners

North Innovation Fund